Can Industry Recognition Strengthen Phreesia’s (PHR) Competitive Edge in Digital Healthcare Solutions?

Competitive Edge in Digital Healthcare Solutions?")

- Phreesia was recently named to the 2025 Capterra Shortlist in both Patient Engagement and Medical Scheduling, reflecting strong client feedback for its digital healthcare solutions.

- This recognition points to heightened market leadership and could further bolster Phreesia’s reputation among healthcare providers seeking advanced digital engagement platforms.

- We’ll examine how this industry recognition for digital healthcare solutions could reshape Phreesia’s investment narrative and growth prospects.

Find companies with promising cash flow potential yet trading below their fair value.

Phreesia Investment Narrative Recap

Belief in Phreesia centers on rising digital adoption across healthcare and the ability to capture value from new, user-friendly engagement tools for providers and patients. While the Capterra Shortlist honor signals growing client satisfaction and could enhance credibility, it does not directly shift the company’s immediate growth catalysts, which remain tied to successful rollout and adoption of new modules, nor does it resolve the main risk of increasing competition from larger, integrated healthcare IT platforms.

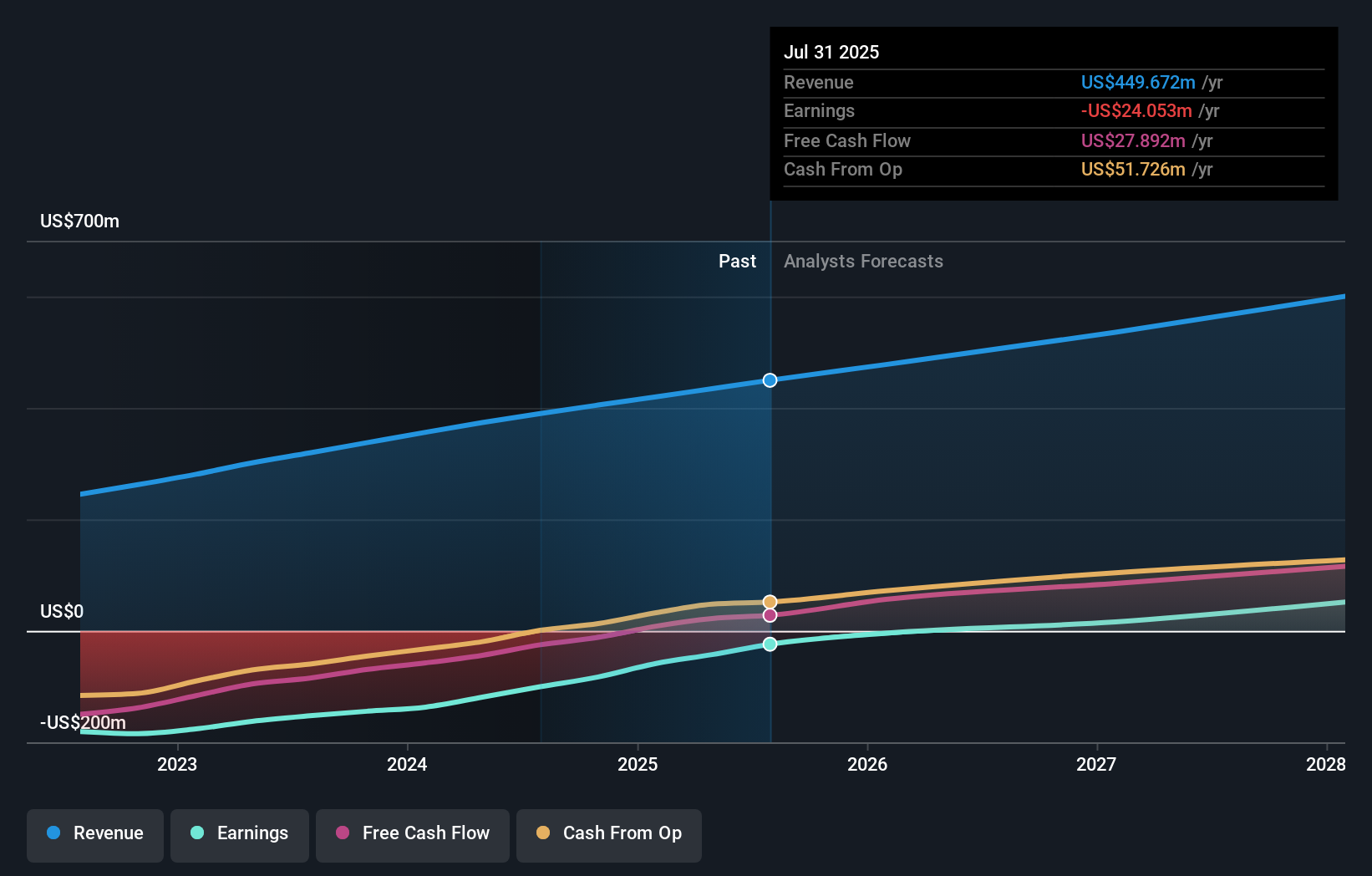

Of recent announcements, Phreesia’s scheduled fiscal second quarter 2026 results release on September 4, 2025 stands out, providing the next tangible read on whether expanding platform capabilities and positive client sentiment are translating into gains in revenue per client and operating leverage.

In contrast, investors should be mindful that as competitors integrate more patient engagement features into EHR and EMR platforms, Phreesia’s differentiation and pricing power could face…

Read the full narrative on Phreesia (it’s free!)

Phreesia’s narrative projects $611.2 million revenue and $51.0 million earnings by 2028. This requires 12.0% yearly revenue growth and a $93.7 million increase in earnings from -$42.7 million today.

Uncover how Phreesia’s forecasts yield a $32.21 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community estimates for Phreesia’s fair value all cluster at US$32.21, reflecting a single but unified private investor outlook. As digital adoption grows, competition from integrated solutions remains a central factor for readers to weigh when considering future performance and opinions can vary, explore several viewpoints before making up your mind.

Explore another fair value estimate on Phreesia – why the stock might be worth just $32.21!

Build Your Own Phreesia Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Seeking Other Investments?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link